Another return of the Watch Series: FitBit (FIT) – dead horse or exciting pivot ?

Watches again…..

Although I wrote a lot about Watch companies over the past few years (Swatch part 1, Swatch part 2, Hengdeli, Fossil part 1, Fossil part 2, Movado, Richemont), no investment came out of it. However I had a lot of fun researching these companies so it was time well spent.

When I initiated the series in 3 years ago, Smart Watches were a big thing and especially the Apple Watch was perceived to be the “Swiss Watch” killer, which, as we know now didn’t happen as they seem to coexist quite well.

Besides Smart Watches, Fitness Trackers were the “hot shit” and especially VC backed FitBit that IPOed in 2015 was taking oer the world.

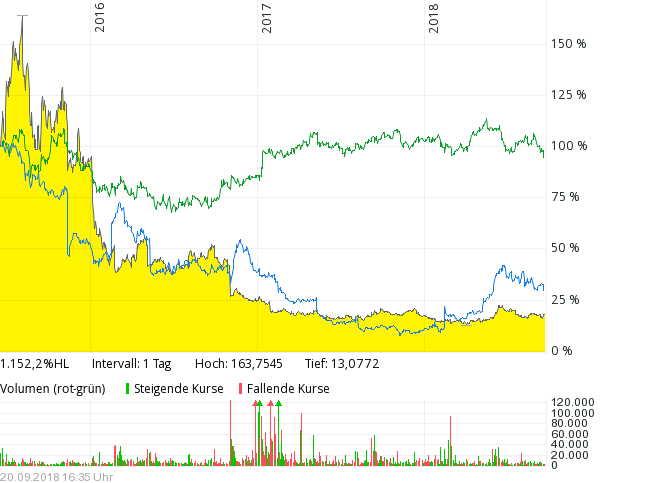

This chart shows Fitbit against Fossil (blue) and Richemont (green) and we can clearly see who had staying power and who not:

FitBit had clearly the hardest time, losing more than 80% from its IPO. It is also a confirmation of one of my “mental model” which says tha “Gadget IPOs” will fail at some point in time, unless they are called Apple.

Why look at Fitbit ? It’s a dead horse…

Fitbit does have a couple of obvious issues:

- low price competition on the Fitness tracker low-end (especially Chinese Xiaomi)

- High end competition from Apple, especially with its latest Apple Watch 4 that also focuses on health application and tracking

- It’s first attempt at smart watches, the Ionic was not very successful

- Q2 2018 looked especially bad from a cashflow side

- Top line sales are still contracting

- Like many “gadget” companies there is a lack of recurring revenue

- The CFO left some months ago

- Tariffs on China imports will hit them (however also their competitors)

What I like at Fitbit:

- the company did not burn cash since its IPO (420 mn raised in 2015) but managed to keep a nice cash cushion

- The founders are still on board, owning significant amount of shares

- The strategic “pivot” towards health data platform makes a lot of sense

- They do have a potentially valuable user base and (still) a very good brand

- The latest smart watch, the Verso seems to be doing quite well

Competitive environment

FitBit clearly has under estimated the impact of smart watches. This is from the latest quarterly report.

Revenue decreased $54.0 million , or 15% , from $353.3 million for the three months ended July 1, 2017 to $299.3 million for the three months ended

June 30, 2018 . The decrease was driven by lower demand for our connected health and fitness devices as consumers continued migrating towards higher-end

smartwatches. The decrease was offset in part by increased demand for our smartwatches, which increased to 55% of our revenue in the three months ended June 30, 2018, compared to the same period in 2017 where we did not sell smartwatches. During the three months ended June 30, 2018, we were also impacted by supply constraints associated with Fitbit Versa which limited our ability to fully satisfy the demand for this product during the period.

As mentioned above, especially Apple tries to position the Apple Watch as a kind of “health device” and it looks like that many people prefer a “smart” watch vs.a “dumb” fitness tracker,

Looking at the Amazon sales rankings, also Samsung is a significant competitor as well as Garmin and a few “cheapies” like “YAMAY” and others.

Nevertheless, the Versa seems to be selling quite well at the moment.

Numbers Numbers Numbers

These are a few numbers I quickly compiled that I found interesting

A few observation from my side:

- The IPO in 2015 was really timed very well. 2015 was just the end of the high growth period. I think what happened is that all the early adopters bought a fitibit device but then it didn’t really go mainstream after that.

- Stock based compensation is edging up. This is no surprise and quite logical: If your stock price doesn’t rise, you have to offer good engineers more stock. This is something that I observe on a regular basis: As long as the stock price is going up, initial compensation is low. But once the stock is falling, grants have to become larger. In my opinion this could become an issue at some point for Google, Amazon etc as well when their stock prices fail to rise.

- R&D spend is increasing significantly, both in absolute and relative terms. This is quite interesting as the natural reaction for a company in a situation like Fitbit would be to slash R&D in order to get back to profitability. FitBit in contrast is pending more and more. This could either be really bad (i.e. spending on devices that fail to sell) or really good (building infrastructure for their health platform).

Trying to become a “health platform”

Just a few days, FitBit however announced something really interesting: Humana, a relatively large US-based health plan announced that they would role out the FitBit platform to around 5 mn plan members. Although it needs to be seen how that is transforming into sales and earnings for FitBit, it is still a pretty impressive achievement.

If this becomes successful (and this is a big IF) this could be really interesting as these kind of revenues are worth much more than gadget sale. A rule of thumb is that the value of anything health data related is around 10 times revenue these days…

To be continued…..

Despite its ugly chart and the obvious issues, I do think that a lot of aspects at FiBit are interesting. So there will be a second post next week.

In the meantime a spared no expenses and got myself a new FitBit Versa and i hope I can also share my first experience.

To me this is far far away from value investor, and fully in the speculative invesment muddy waters. In other words: anti-Buffet.

And then what ?

Do you consider Berkshires latest India Investment as Anti BuffetT, too ?

https://www.forbes.com/sites/gurufocus/2018/08/27/berkshire-hathaway-takes-stake-in-indias-paytm/#5c77b4874984

1. Seems the transaction is not Buffet driven.

2. The latest Buffet (2000-2018) is not greatest Buffet (pre-2000) which is the one everyone (you the first) admires.

3. I also note that Payment intermediaries (Visa/Mastercard and lately Paypal/Amadeus & the StockExchanges) were always favourites among the best outperforming managers, because of their high-ROCE and high operating margins. See Fundsmith (or Buffet itself whose largest position is American Express).

Trying to get an edge into the future of payment intermediaries (and industry where high Roce is commonplace) I find it FAR LESS specualtive than investing in a ‘glorious’ company like FitBit whose glory lasted two seasons, and whose resemblance to Blackberry/TomTom scares me. I wonder what are the operating margins & Roce of FitBit and of its peers.

Yet, I will not hope for turnarounds but, (as Buffet) I will keep investing in high Roce / Operating Margins companies with higher predictability (large number of small regular transactions). And I have a nice shortlist.

Just one remark here (more in a post): Buffet is the place to eat whereas BuffetT is the name of a famous investor …..

I think the most interesting aspect with FitBit is this: https://www.theverge.com/2018/9/26/17905390/john-hancock-life-insurance-fitness-tracker-wearables-science-health

That would open a market of tens of millions of devices, and there would be recurring revenue if FitBit manages to collect additional data with new trackers/watches.

What’s also interesting – when you do a news search for something like “insurance company fitness data”, you end up getting many headlines that include “FitBit”, such as “Should you hand your Fitbit data to an insurance company?”, but no other smartwatch-producer is mentioned.

And I would add that ECG/EKG coming to the next Apple watch.

This will be the new standard and benchmark.

Now Apple acquired a patent years ago. I wonder where everybody else stands on this (Garmin, Polar, Fitbit…)

I know some PE shops were circling AliveCor last year.