Some thoughts on High Interest Rates and Financial Services Companies (Silicon Valley Bank, Commerzbank)

For some time now, many market pundits were pushing the idea that Banks and Insurance companies would be basically “no brainer” investment as higher interest rates mean higher profits for these players.

And indeed, historically one can observe that higher interest rate levels allow for higher spreads, both for banks and insurers. Subsequently, even low quality institutions like Deutsche Bank and Commerzbank saw decent rises in share prices, even significantly better than the respective indices:

The main problem: existing assets and liabilities

The main problem however with the “higher interest rates are good” for banks and insurance companies is the fact, that they cannot start from a clean sheet. Every financial institution has a starting Asset pool and liability structure. Increasing interest rates eat themselves through the financial system at a relatively slow but unstoppable pace and different mismatches will be revealed at different stages during that process.

Early victims: Liquidity mismatches

The earliest victims will get caught if the underestimate the liquidity of their liability side and are then forced to liquidate assets at (very) unfavorable prices.

First “Liquidity risk victim”: Uk Pension funds

Very early in the current interest rate cycle, we saw the first casualty: UK Pension funds, which used large amount of derivatives in order to extend their asset duration which in turn led to high collateral requirements and forced sales of liquid long term governemnt bonds which in turn pushed interest rates higher. Only a massive intervention from the Bank of England prevented that UK meltdown. In the case of the UK Pension funds, the potential liabilities of the derivatis were not adequatly matched with uncorrellated liquid assets which caused the systemic problem. Due to the instant collateral requirement, the problem surfaced very early in the crisis

Second “liquidity risk” victim: “Liquid real estate funds” Blackstone

Blackstone, the US PE giant had arount 70 bn USD in real estate funds that invested into illiquid real estate but offered investors to get their money back at regular intervals. As the prices for the funds still went up, some investors thought it might be better to get the money out which in turn required Blackstone to “gate” withdrawels. In this case, Blackrock had actualy the opportunity to stop withdrawals, which in the short term of course helps them a lot, but in the mid- to longterm will create some reputational issues with their investors.

Third “liquidity risk victim”: Silicon Valley Bank

In a situation that is currently developing, among other issues, Silicon Valley Bank thought that it was a good idea to invest a significant part of short term deposits into long term Mortgage Backed Securities (MBS).

This week it seems that its institutional depositor base seems to have became worried and satrt to ask for their deposits which in turn will require SVB to sell thes bonds at a loss and therefore deplete capital which could easily turn into a death spiral in a few days.

It will be interesting if and how the situation develops over the week end. My best guess would be that a few Silicon Valley VCs/Teck billionaires might step up and rescue SVB as the Bank is super important for the Silicon Valley ecosystem.

The market now will clearly try to identify and “hunt” banks that have similar mismatches. I could be very wrong, but I do think that most of the larger players, both in the US and Europe have managed their liquidity risks a lot better than SVB, but some smaller and more “innovative” players could be equally vulnerable.

Mid- to long term victims: Credit troubles – Example Commerzbank

However, liquidity risk is something that usually shows up at the early stages of an interest rate cycle. The other, much slower but at least equally big risk for any financial institution is credit risk. Higher interest rates mean higher expenses for borrowers. Over time, more and more highly leveraged borrowers will start to default. For banks, in principle this could be manageable, as the usually have collateral that they will seize and sell. But if the collateral is also negatively effected by rising interest rates (e.g. real estate), another death spiral could be created.

The credit cycle normally moves a lot slower than the initital liquidity cycle and to be clear, for the last 20 years or so there was actually not a “real” credit cycle. The first credit cycle, after the financial crisis was mostly mitigated through central bank intervention. The second potential cycle following Covid was neutralized via direct transfers from the Government. I think it is fair to assume certain interventions again this time, but it would be very optimistic to again assume no real credit cycle this times with high fefault rates over a couple of years.

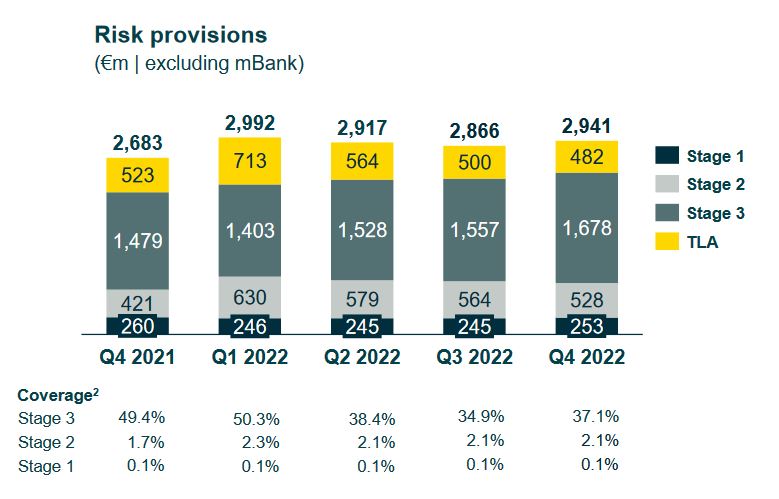

Interestingly, some banks seem to see this very differently and do not prepare themselves for a more harsh climate. Commerzbank for instance, who proudly reported “record results” for 2022 did not increase loss reserves very much in 2022 as shown in this slide from their investor presetnation and seem to cover their existing exposures at a lower level than at the end of 2021:

This clearly allowed them to increase compensation for Managwment significantly but I do think that there is significant potential for nasty surprises in the next few years. Commerzbank might be facing increasing write-offs in the very near future if more creditors get into trouble and therfore I find it very aggressive to actually lower the coverage of the existing exposure.

Interestingly the mortgage sector for them is not a concenr, as they write the following:

The automative sector however, who just recorded record profits, is mentioned as a risk sector. I am not saying that Commerzbank is the worst offender, but assuming that it can only go up for them from here due to higher interes rates is very naive. Maybe Commerzabnk can create one good more year if the credit cycle moves slowly or interest rates would go down quickly, but at some point in time they have to face reality.

So when looking for potential financial services companies to invest, one should look especially if and how and institution prepares for the coming necessary adjustments.

Summary:

In my opinion, we are currently in the early stages of a longer adjustment process that high interest rates will be “adequatly reflected” on the balance sheets and the P&L of financial companies. This adjustment process will very likely lead to significantly higher default rates than we have seen in the last 20 years which in turn is a big issue for every financial institution.

Those companies who had conservative balance sheets before this recent devlopment and prepare themselves with adequate provisions will have much better chances of being long term winners than those who do not.

One should be especially careful with companies that were already in troule before interest rates shot up so quickly (Credit Suisse for instance).

Be careful, stay safe !!!