All Swiss Shares Series Part 4 – Nr. 31 – 40

Another week, another 10 Swiss stocks, this time with one stock to “watch”.

31. Plazza AG

Plazza is a 581 mn CHF market cap real estate company that invests in and around Zurich. The company seems to trade close to NAV and as a rule I normally don’t consider listed real estate as part of my investment universe, therefore I’ll “pass”.

32. Komax AG

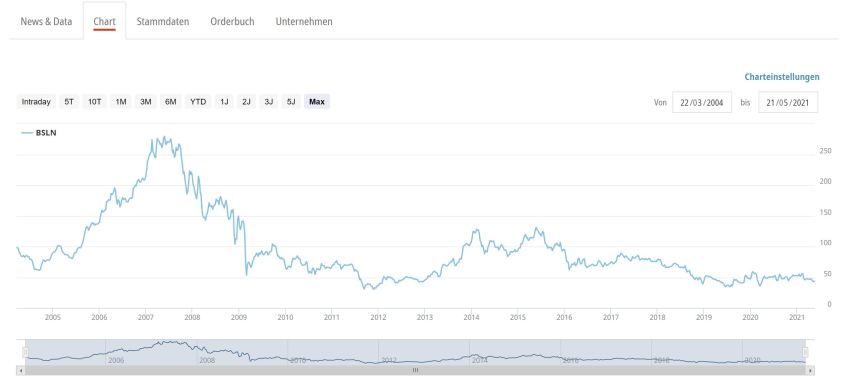

Komax is a 831 mn CHF market cap company that supplies cable automation machines to mainly car manufacturers but also the Aerospace industry as well as other industries. As a automobile supplier, business suffered already in 2019 before getting hit again in 2020.

The stock chart shows a significant cyclicality which is not a surprise: