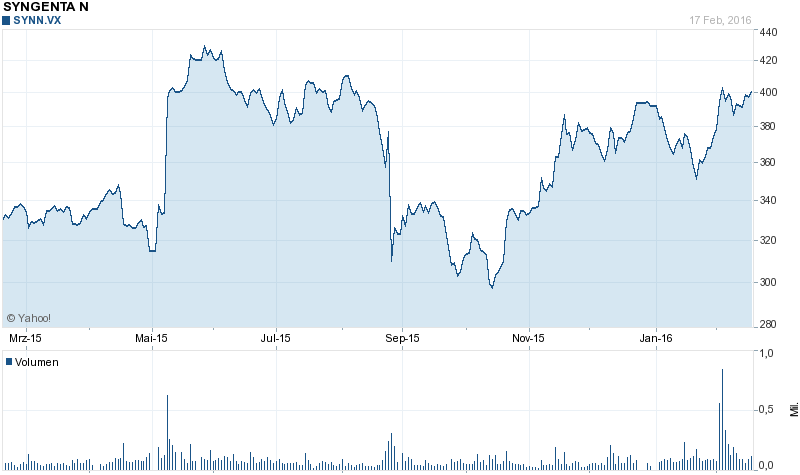

Syngenta ChemChina offer

After the failed attempt of Monsanto to buy Syngenta last year, Chinese conglomerate ChemChina made an offer for Syngenta a couply of weeks ago. Other than with Monsanto, the Syngenta board already approved the take over.

The offer itself is as follows:

ChemChina will pay 465 USD. On top of that, anyone who buys Syngenta shares now, will receive the normal dividende of 11 CHF and a 5 CHF special dividend.

If we expect closing at the end of the year, the potential return would be (in CHF) at a current price of 400 CHF:

-400+(465*0,994)+11+5= +77,75 CHF or a potential 19,4% return for 10 months.

This looks very attractive. However the merger arbitrage/event market is a very competitive one and those spread usually don’t come “for free”. So why is there such a large spread ?

US regulatory risk

I guess the most obvious reason is that investors fear that US regulators will try to kill the deal. Syngenta has a signifcant US business. There are several rumors around why the US authorities might challenge the deal, most recently some in connection with the Zika Virus.

The Committee on Foreign Investment in the US (CFIUS) will review the deal because Syngenta, through its US research and production facilities, plays a key role in the US food industry.

The Zika virus problem could force CFIUS’s hand, sources said.

“CFIUS focuses solely on whether an acquisition represents a national security risk,” a Beltway CFIUS expert not involved in the merger told The Post. “I certainly think Zika will be a factor.”

From what I found on the net, the problem is that the CFIUS never really explains their actions, so it is very difficult to judge as an “amateur” what the chances will be. A professional hedge fund clearly has the money to pay for advice, most likely from former members of the CFIUS. This is clearly an information disadvantage form me as small investor.

China FX issues

Another problem I could see is the fact that ChemChina needs to come up with around 44 bn USD in USD financing and this could be difficult if there would be really turmoil in China in the meantime.

They haven’t even refinanced their Pirelli bridge loan yet and at least in the Pirelli case they don’t seem to guarantee those loans:

The new refinancing will be non-recourse to ChemChina, but will have elements of support from Pirelli’s Chinese owner, bankers said.

So I guess the ~20% discount is basically a mixture of regulatory risk and financing/China turmoil risk.

On the plus side, even if the ChemChina deals would fall through, there still could be other players interested such as German chemical Giant BASF.

Is Syngenta then an interesting special situation investment ?

What is bothering me is the following: As I said before, this area is very competitive and Syngenta is a liquid stock (50-100 mn CHF a day) and I do not have any special insights into the situation.As discussed before, I guess I have even an information disadvantage.

The potential downside for a failed bid is at least -25% when we look at what happened after the Monsanto bid:

So if I assume a simple 50/50 probability, my expected value is negative.

Every “event driven” fund is clearly looking at Syngenta which in turn means that they seem to price the risk at the current price and assume a slightly better chance than 50%.

However I clearly have no basis to assume any higher percentage for a succesful outcome.

All in all, in the past it never had paid out to invest into such a situation with an information disadvantage, so I will stay away from this one.