Panic Journal 2026 Spring edition – Trump/Iran, SpaceX/Indices and German NatGas storage problems

Disclaimer: This is not investment advice. PLEASE DO YOUR OWN RESEARCH !!!

Time for another “Panic Journal” episode after the last one is already from one year ago. Writing about this is for me the best way to structure my thoughts and maybe it is of interest for some of my readers, too. Towards the end, there is even some kind of “actionable” content, too.

Trump/Iran:

I think the best advice on how to react to whatever Trump is saying is not to try to time anything here. As German “Finfluencer” Christian W. Röhl keeps saying (freely translated): “If you always react to what Trump is saying, you won’t make money, you just become (equally) insane”.

Last year, this was about Tariffs, then it was about Greenland and now it is about Iran. Who knows what is next. Maybe attacking Australia for some reason ? Who knows.

From a more strategic perspective, the narrative that the Trump administration is “good for business and the economy” seems to be now permanently broken.

Yes, Corporate Taxes in the US are lower, and Mr. Trump wants the stock market to be up “bigly” but the uncertainties around tariffs, “ideologically” driven crack downs on immigrants, careless international relationship management and potentially even much larger government deficits due to increased military spending are slowly showing their impact.

Another example: The White House has been celebrating net negative migration yesterday, but population growth has been one of the distinct drivers of US growth in the past, mainly through “household formation” especially compared to Europe or Japan. I guess this tailwind will have disappeared already, along with the immigrants who actually are supposed to build the houses.

Maybe, but only maybe, the AI build out can compensate for all of this, but maybe not. My very subjective impression is that the famous “American Exceptionalism” for stocks seems to be depending now fully on the success of AI. Which I think is quite risky. The annual letter from Bireme Capital, to which I had linked to captures most of this and more.

SpaceX/Indices

As my readers know, I have actually a small “side bet” on the SpaceX IPO with my position in Rocket Internet. Now more and more details become available about how this will work.

Basically, Elon wants to take SpaceX public at a valuation of 1,75 trillion after merging it with XAI. The valuation is roughly 100x revenue. Two details that I find interesting are:

- Elon wants to allocate 30% or more of the 75 bn offering to retail investors.

- The index providers, in this case Nasdaq will grant an exemption and potentially allow SpaceX to enter the Index already after two weeks instead of 1 year and are waiving free float requirements

- In addition, I read that SpaceX weight in the Index could be up to 5x bigger than its free float would justify.

The game plan is pretty clear: Give as much as possible to Elon’s “price-insensitive” fanbase and then force the index funds to “fight” for the little free float available and allow the insiders an easy exit at the proposed nosebleed valuation.

But what does that mean for index investors for the future ?

As an index investor in the past, the big advantage was that you automatically caught the big winners rather early.

Nvidia for instance entered the Nasdaq 100 in May 2001 at a share price of ~30-40 ca and a market cap of around 6bn USD.

So a long term index investor participated fully in the 400-500x over the last 25 years. Same with Google, Amazon and all of the other big winners that drove past index gains. Even Meta IPOed “only” at a market cap of ~100 bn in 2012. That’s the reason why the Nasdaq100 returned around 16% p.a. for the last 20 years and making a lot of people very wealthy.

SpaceX is the first member of the “new breed” of IPOs where most of the value accretion basically happens outside the listed stock market in the private markets. As an Nasdaq Index investor you will be forced to allocate a significant part into this company at a much later stage and at a much higher price.

And SpaceX is only the first candidate of that new breed. OpenAI, Anthropic, Anduril, Stripe are other candidates that might go public at valuations at hundreds of billions or ven trillions.

It is very likely that Index investors will participate (if at all) at a very late stage of the success of these companies. The conclusion is relatively simple: The more such IPOs and “quick entries” happen, the higher is the risk that Index investors will not be able to earn the returns that they did in the past when these companies entered the indices much earlier. There are clearly other factors that influence returns as well but this one could become quite significant in 2026.

German Natural Gas storage / Renewables

In the big scheme of things this is a small topic but clearly personally relevant for me. Natural Gas is a very important source of energy in Germany. We need it for the industry, to generate electricity and to heat homes. Due to German weather, demand is much higher in Winter than in summer. Therefore, Germany has created significant Gas storage infrastructure that is able to store up to 3 months of peak WInter demand. I don’t need to stress that only a very small percentage of demand can be met with local resources.

The relevance of that storage became clear when the Russians first throttled the gas pipelines in 2021 and then Northstream II was blown up in 2022.

This led to panic buys of the then Green Ministry of economics in 2022 which in turn led to record high gas prices in 2022.

Following those events, the German Government introduced some minimum requirements for gas storage plus incentives for utilities to buy natural gas in advance and compensate them if they have to sell it cheaper later on.

The new German Government under the the Economics Secretary Katharina Reiche (former employee of utility Eon and supposedly an Energy expert) however decided that those incentives are not needed anymore in 2025 and expected that “the market will solve this” and lower the costs for the Government (and tax payers/consumers).

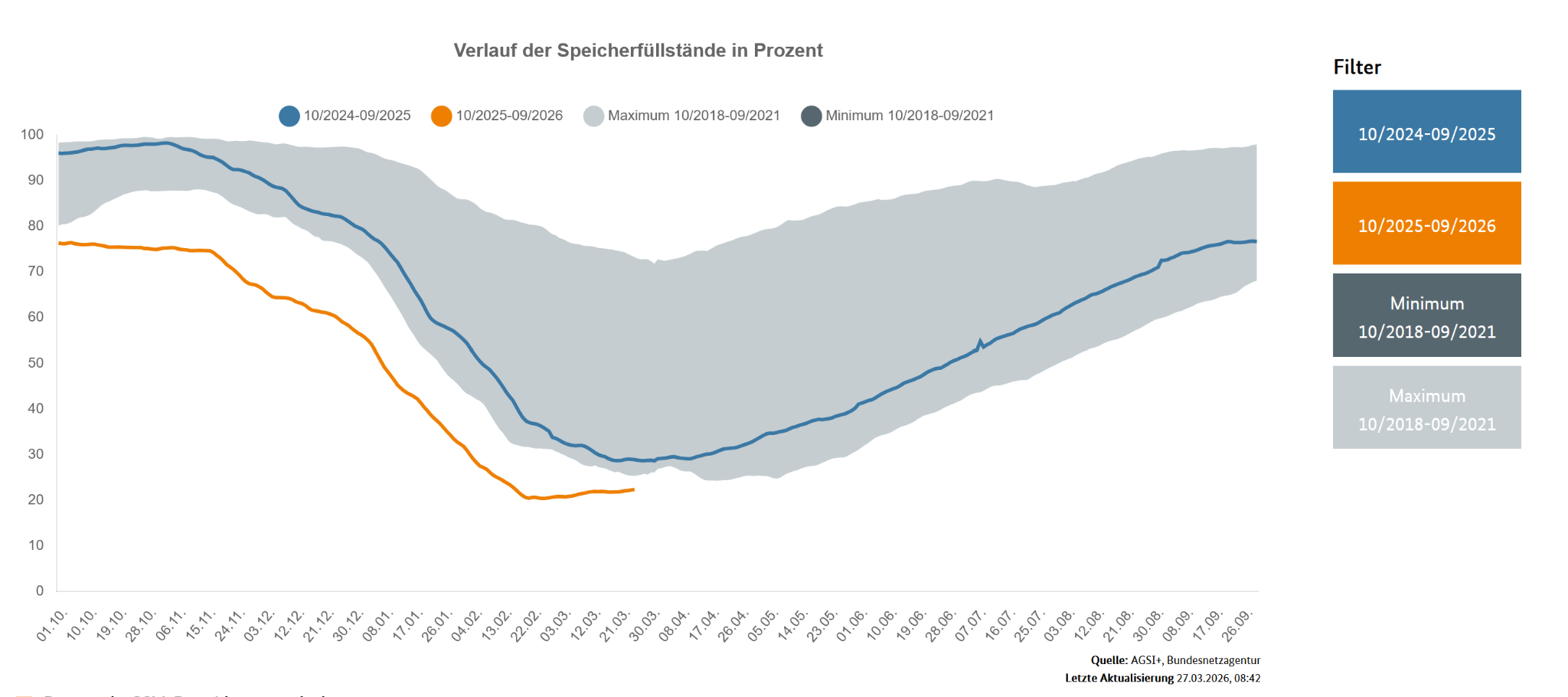

Fast forward to End of March and the market “solved” it in a way that despite a relatively mild winter, gas storage levels are at a record low of 20% as this chart shows:

Now as we all know, the supply of global LNG is pretty handicapped, as Qatar has shut down its facilities which took around 20% of global capacities off the market. Some of that seems to be now permanently damaged.

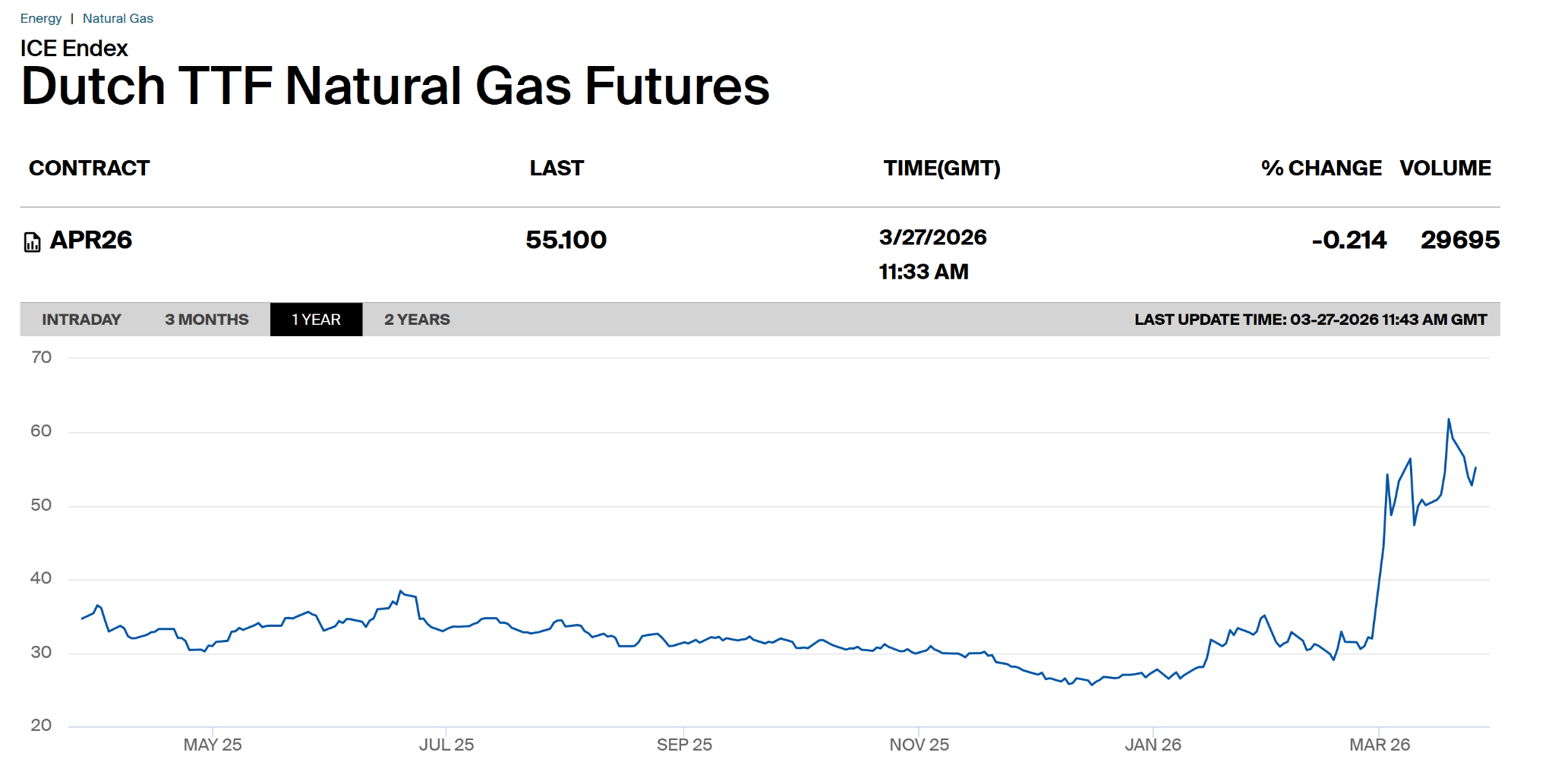

Although natural gas wholesale prices in Europe came down a little bit over the past few days, they are still 80-100% higher than end of last year or beginning of this year:

Of course, the incentive of the utilities to fill up gas reserves without any help right now is zero.

Back in 2022, Mr. Habeck started buying Natural Gas with Government money in the beginning of March when storage levels were at 30%. This time around, Ms Reiche is still only “monitoring the situation” 4 weeks later at a much lower level of reserves.

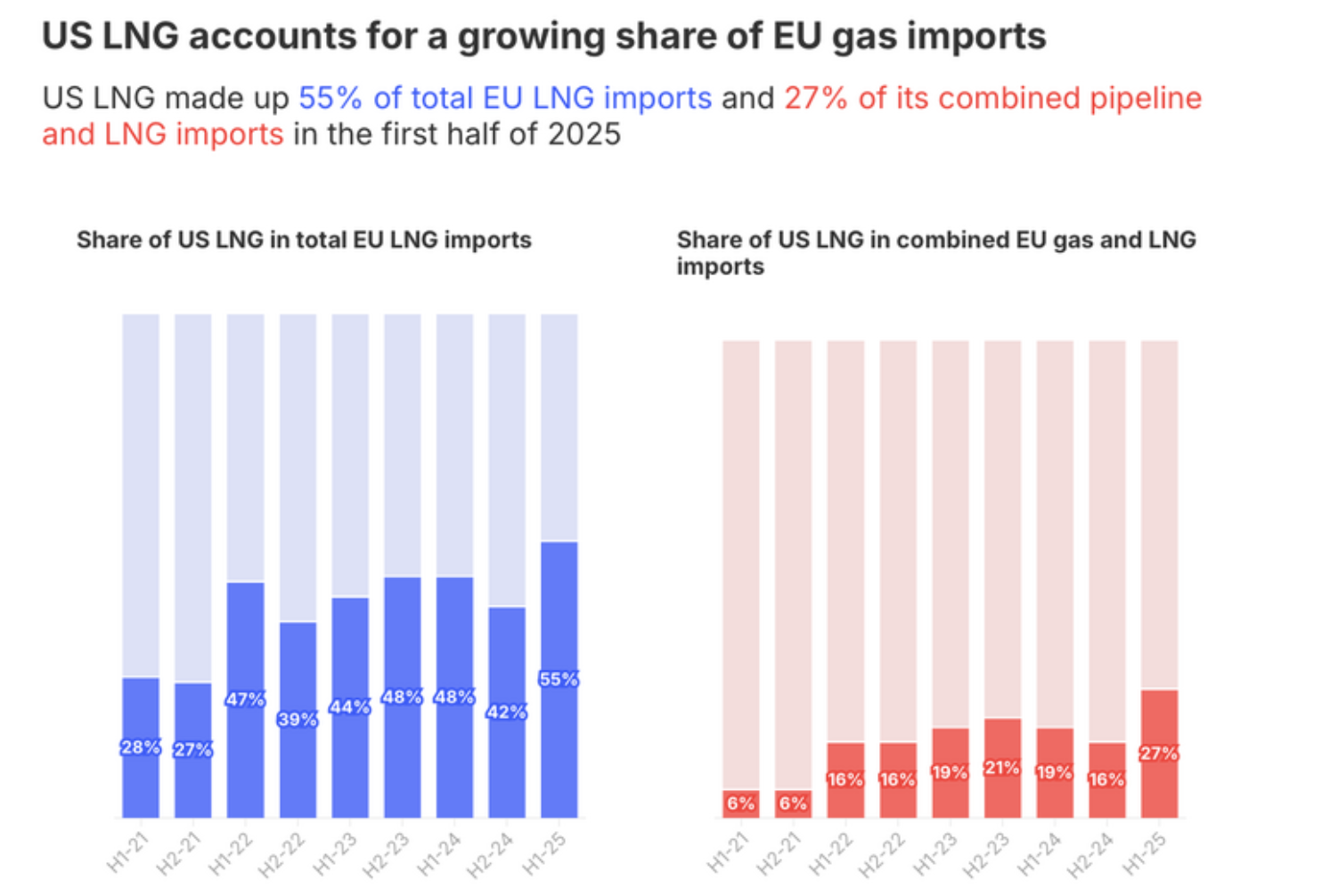

With the global shortage of LNG, it has clearly not become easier and cheaper to fill up German storage levels. Since 2022, Europe is relying much more on US LNG imports as this chart shows:

But Mr. Trump would not be Mr. Trump if he would not already threaten Europe repeatedly with stopping LNG exports if Europeans do not behave the way he wants us to behave.

To top things up, Ms Reiche is planning to phase out subsidies for Renewables and also make life more difficult for battery energy storage according to some leaked documents and focus even more on gas fired infrastructure for electricity generation in the future.

So what does all of this mean ? In my opinion this means that energy prices might stay higher for longer and the risk of a “panic reserve buying” spike like in 2022 is increasing.

As the price of natural gas is also driving the price for electricity, everyone who uses electricity has some significant risk that these bills might rise significantly in the coming weeks/months.

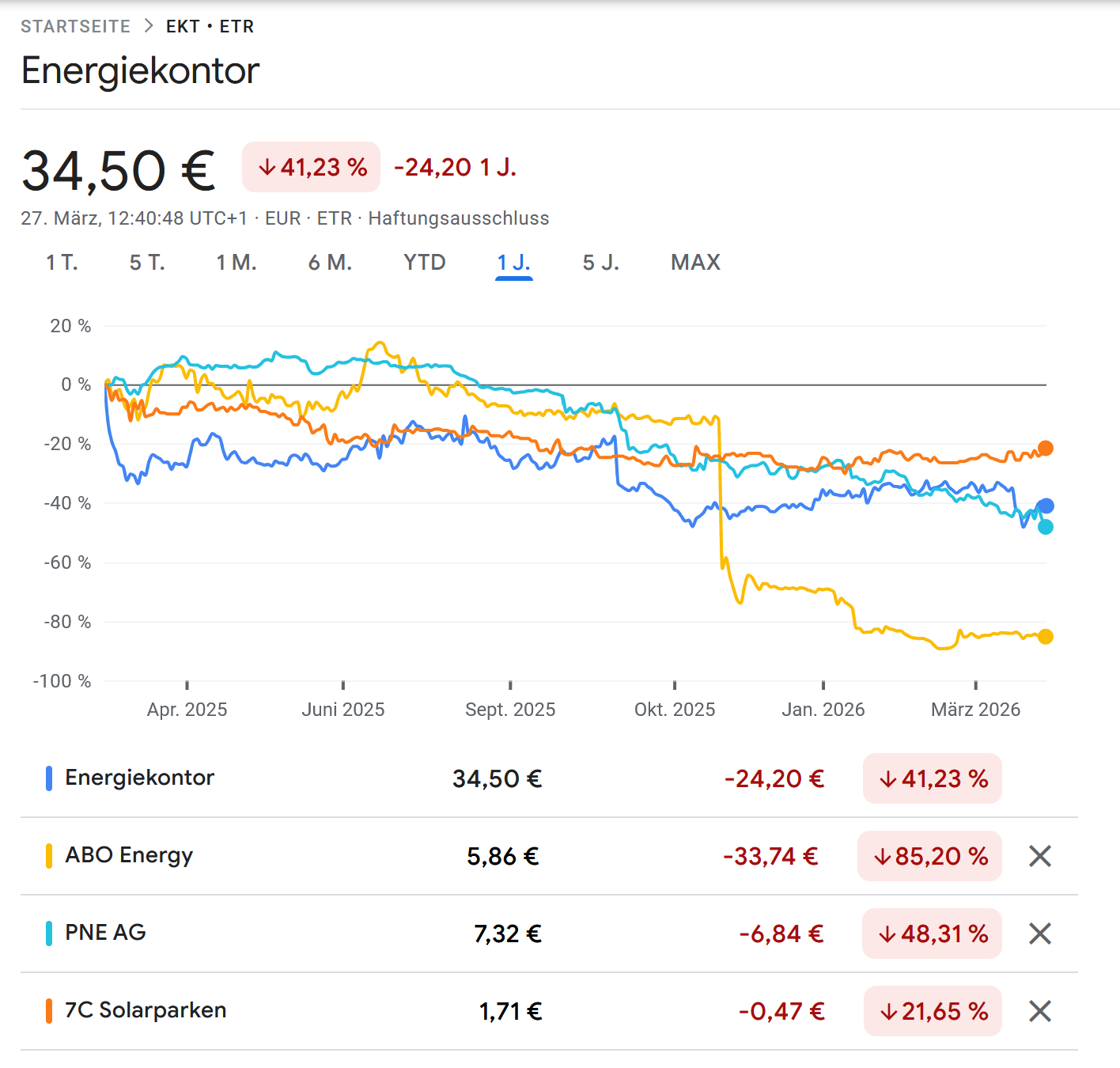

Back in 2022, this led to a short lived boom of renewable energy stocks. Interestingly, so far this hasn’t happened. Here are the stock prices of the main German players which look very depressing:

Especially developers look quite ugly, as their “development pipelines” have been hit massively by oversupply, higher interest rates and generally more negative sentiment.

Interestingly, for many electricity clients in Germany, the bill has decreased this year as the Government has been taken over the cost for electricity transmission and is paying the TSOs directly (among them the former employer of Ms. Reiche).

Overall, the sentiment vs. renewables is really bad with a lot of especially the developers struggling to keep afloat.

To be honest, I have no idea what the future will look like for developers, but operators of renewable energy plants might have some “upside optionality” in this environment.

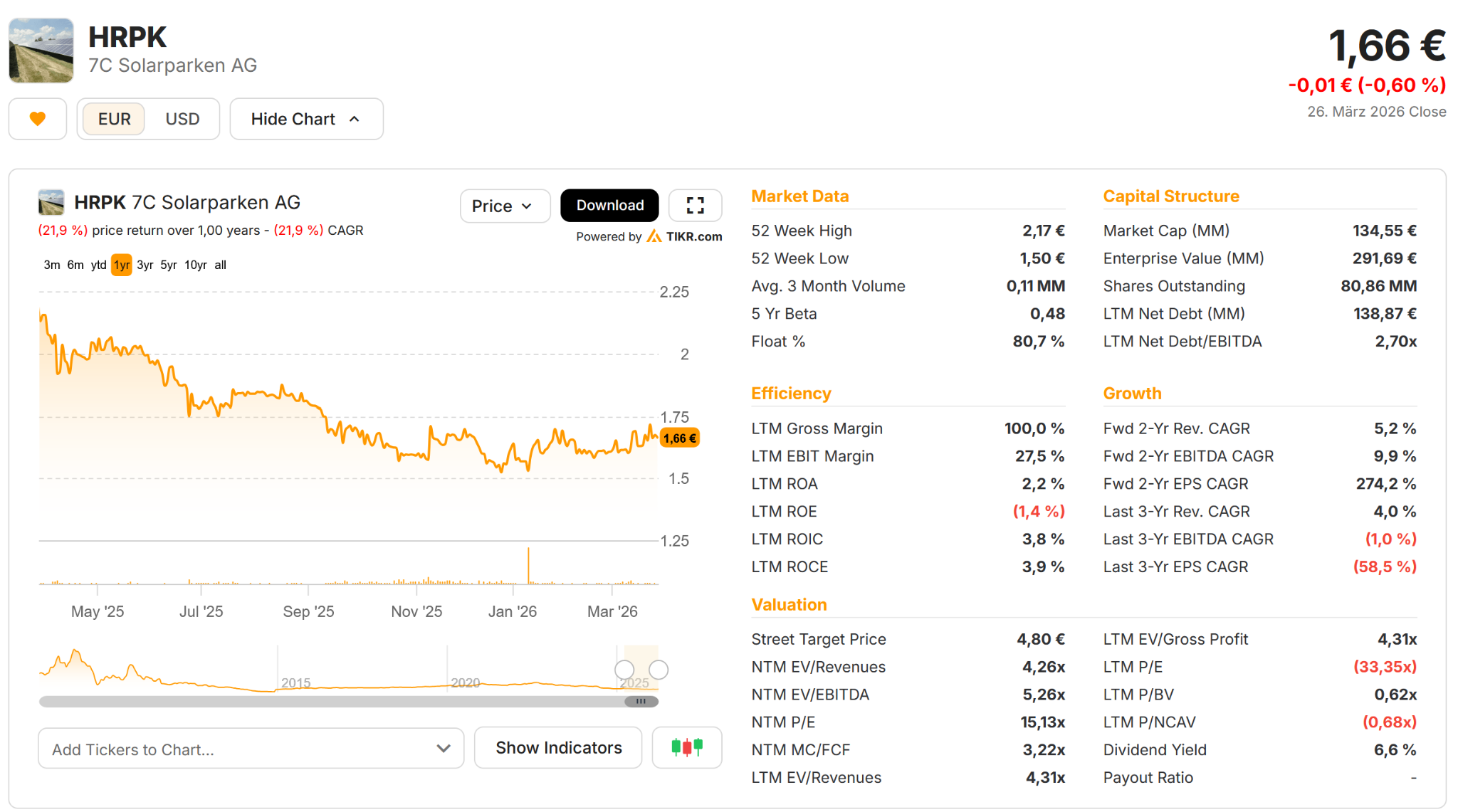

So mainly in order to hedge my personal electricity price exposure, I decided to buy a 1,5% position in a small German Solar PV operator called 7C Solarparken. /C Solarparken was already part of my 2022 “Freedom Energy” basket. They have decent exposure to potentially rising electricity prices and the stock is really cheap ~5x EV/EBITDA and 0,6x book value. They have very little exposure to development projects and generate tons of cash.

Structurally, they also will benefit from less renewables development activity going forward, as every new PV plant cannibalizes existing ones to a certain extent.

This is clearly not a long term growth play but rather a 6-12 month “hedge” in case our Government fuxxs up the refilling of the gas storage during the year, which I see increasingly probable.

Bonus soundtrack:

Who would fit better to my “Panic Journal” than Hamburg legend Udo Lindenberg and his “Panic Orchestra”. Here, an early song from him called “Andrea Doria”: