Hannover Re: An overlooked Reinsurance Compounder & Comparison with Munich Re

Spoiler: This rather long post contains no actionable investment ideas.

Background:

Hannover Re is a stock that for some reason I have ignored for some time although I consider Insurance stocks as part of my circle of competence. Why did I ignore them ? I was always put off from the ownership structure. Hannover Re is majority owned by Talanx, which itself is also listed. Talanx again is owned ~80% bei HDI, which is owned by …I don’t know.

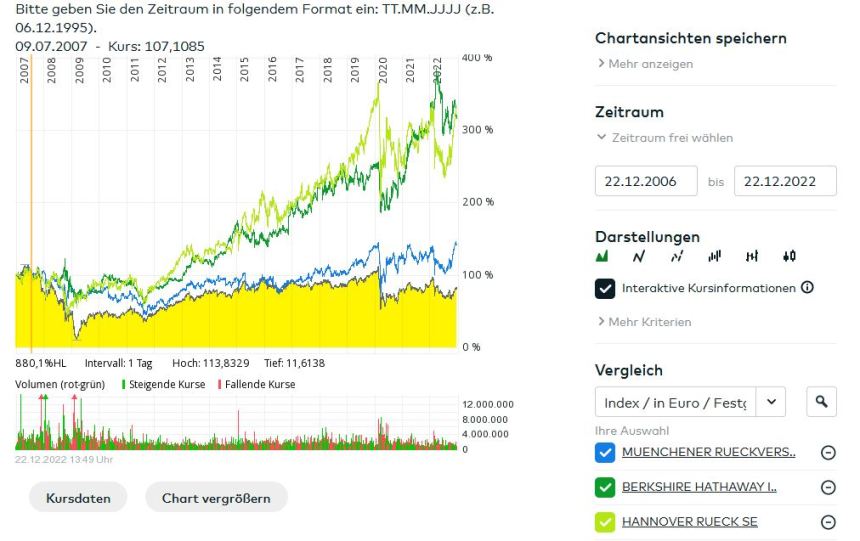

Looking at the chart, I should have considered them earlier: Over the past 15 years, Hannover outperformed the larger and better known peers like Munich Re and Swiss Re by a wide margin and ties with Berkshire (before FX):

This is very interesting, considering that Hannover Re is only the No. 3 global Reinsurer and Berkshire only number 5. Absolute size doesn’t seem the drivig factor for shareholder returns in the Reinsurance industry.

Deep dive Comparison: Hannover Re vs. Munich Re