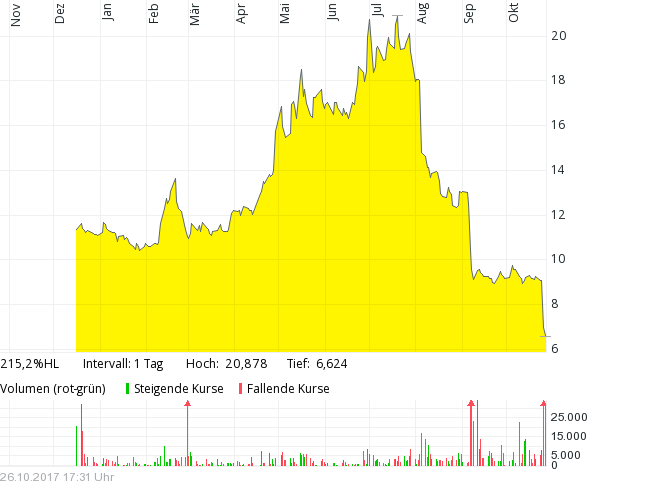

FitBit (FIT) follow up: Enough upside to justify the risk ?

DISCLAIMER

This is not investment advice. Please do your own research and don’t follow any anonymous bloggers.

Let’s continue with this nice “anti Buffett” stock from my post last week.

The people / founders

FitBit’s original founders from 2007, James Park and Eric Friedman are still on board.

Interestingly, although both ar only 41 years old, FitBit was the third company they founded together.

The other companies were Windup Labs, a photo sharing company they sold in 2005 and Epesi, a B2B software company that didn’t work out.