Listed Venture Capital part 3 – The “Tale of the two Vostoks” & UK Vehicles

Background:

Back in the good old days (2018) when Venture and Growth investing were still sexy, I looked into the world of “listed Venture Capital”:

Part 1: HOW TO INVEST INTO VENTURE CAPITAL – LISTED VEHICLES (PART 1)

Part 2: HOW TO INVEST INTO VENTURE CAPITAL PART 2: AUGMENTUM, VOSTOK & OTHERS

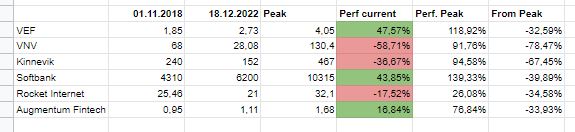

Inititally I bought into Kinnevik, Vostok New Ventures (renamed to VNV) and Vostok Emerging Finance (now VEF), however, I sold both Kinnevik and later VNV (at smallish profits) and only held onto VEF. This is how the Group has performed since then (november 2018) (Prices in local currency only, no dividends/Spin-offs):

Unfortunately I could not find continuous comparison charts for VNV and VEF, but almost all of the stocks at first struggled in 2019, only to go bonkers in late 2021 and then crumble in 2022.

Initially I cursed myself for selling too early , but now it looks super smart to only keep one that is a “winner”.

The tale of the two “Vostoks”: Why so different ?