Paul Hartmann AG (DE0007474041) – Back to my (boring) roots

The company:

Paul Hartmann AG is a 200 year old German company active in the healthcare sector, This is how they describe themselves:

The company:

Paul Hartmann AG is a 200 year old German company active in the healthcare sector, This is how they describe themselves:

The company:

![]()

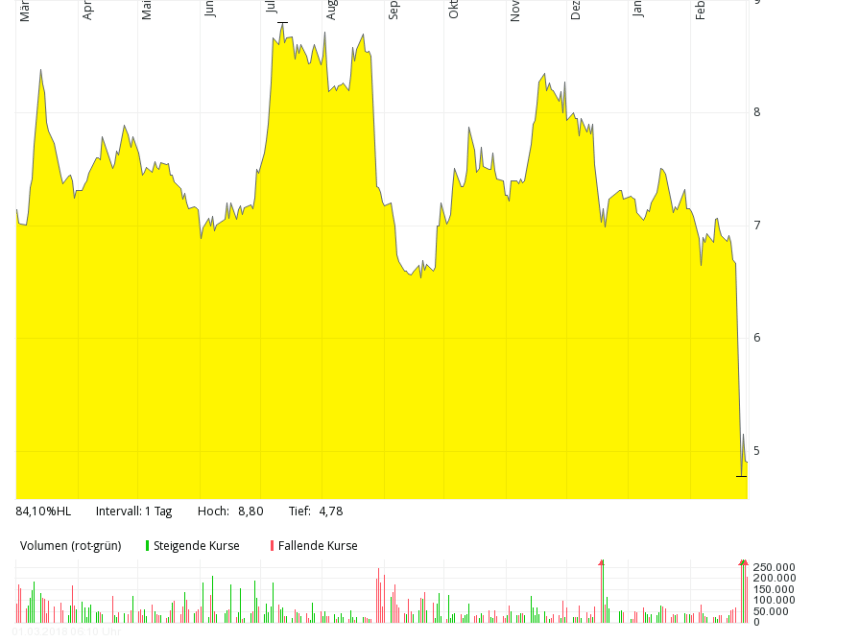

Criteo is one of the few Non-US success stories in the Tech sector. Criteo was founded in France in 2005 and quickly became one of the leading “Adtech” companies in the world. Criteo successfully IPOed 2013 on the NAsdaq and quickly reached a market cap of more than 3 bn USD.

The business:

Criteo is an “Adtech” company. What it does is the following: It is primarily a tech version of the classical Advertising Agencies: Clients use Criteo to maximise the value of their online ad dollars spent which should turn into as many clicks and sales dollars as possible.

A quick update on the Metro case. This is how I ended the Metro post from a few days ago:

For me, it is currently too early to do something. It is not clear to me if the stock price has overreacted or if more trouble is coming along especially from Russia.

Selling now would be clearly an uninformed decision as well as buying more. The next step will be the release of the 6M report next week. I think I will then still wait and see how Russia develops. If, for instance there would be a further profit warning because of Russia, then this would be a clear sell signal.

So let’s quickly check out the half-year report.

The good:

The bad:

The ugly:

The company:

Saga Plc is a UK company that combines two business that I have looked at quite often: Insurance and Travel.

Saga has its origin as a Seaside Hotel in England and then became a travel company before then moving into insurance in the 1980s. Saga caters specifically for the “over 50” market and claims to be the “leading provider” to people over 50 in the uK.

After a PE financed management buyout in 2007, he company was IPOed in May 2014 at a price of 185 pence / share.

Looking at the stock chart, IPO investors at first saw a decent outperformance before things went south this year:

Electrica is the only remaining “Emerging Market” stock in my portfolio. I bought the stock in December 2014 and now after 3 year and some months it maybe time to assess how the situation looks against my initial expectations.

Including dividends, the stock is up ~18% in total since then, in my portfolio however the stock is flat because I bought more of Electrica at higher prices. Compared to a +53% performance of the portfolio in the same period, the stock is clearly a underperformer and the question is clearly if I should keep the stock.

My initial thesis relied on the following assumptions:

What happened ?

During my Silver Chef “Post mortem” some days ago, I decided to look at the 10 biggest losses I made since I started the blog in order to check if I have actually learned from mistakes.

These were the (by absolute performance) 10 worst investments in the 7+ years of Value and Opportunity:

10. Medtronic -18,93% (2011)

Medtronic was one of the initial portfolio investments. I kicked them out in August 2011 as I was not very comfortable owning US large caps and I never deeply looked into the company myself. Medtronic since then outperformed the S&P 5000 IN USD terms (~17,1% p.a. vs. 15.3%) or ~ 233% in EUR terms. This is slightly better than my portfolio which made around 215% in the same period.

A few days ago, Silver Chef came out with their half-year update. There is the glossy half-year 2018 Investor Presentation and the 2018 half-year report.

Looking at the stock price, the market clearly didn’t like the news very much:

So what happened ?

Disclaimer: This is not investment advise !!! Do your own research !!!!

The guy who wrote this post just lost a lot of money with his Silver Chef position. You might even consider shorting his recommendations 😉

Background:

When I looked at Expedia almost exactly one year ago as part of my 2017 Travel Series my key take negative aways were as follows:

– CEO has super high salary (90 mn USD in 2015)

– top line growth, operating profit stagnant

– expensive acquisitions in 2015/2016, number of shares and debt increased significantly

– reported growth numbers not adjusted for acquisitions in investor presentation

– lots of share options

Additionally, the stock looked expensive:

At 119 USD per share, Bloomberg tells me that they have a trailing P/E of 54, an expected 2017 P/E of 22,3 and an EV/EBITDA of ~16. This means that a lot of growth is already priced in.

As we can see in the chart, the stock became at first even more expensive before dropping back to a level of around 100 USD / share:

Background

![]()

Landis & Gyr, the Swiss based company was on my research “to do” list for some time. Why ? Because it looked very much like a “forced IPO” special situation when in Summer 2017 then almost bankrupt Japanese Conglomerate Toshiba decided to sell Landis & Gyr which was deemed to be one of their crown jewels.

Toshiba itself had bought Landis & Gyr in 2011 for around 2 bn USD from a Private Equity Seller (Bayard) who in turn had bought Landis & Gyr from KKR (via DEMAG), another PE shop in 2004. Back then, Landis & GYr had around 390 mn EUR in sales and it was rumoured that the purchase price was quite low at around 100 mn EUR (those were the days…..).

A couple of days ago, I looked at Softbank more from a strategic point of view. This time I want to focus more on the actual assets and a sum-of-parts valuation

What is Softbank ?

Essentially the company at its core is a Telco company in Japan and US plus a lot of “extra assets” like the Alibaba stake, Yahoo Japan and then all the other stuff including the vision fund. The initial Software distribution business (this is where the name Softbank comes from) doesn’t play a big role anymore.

I will now try to walk through the major Softbank Assets in more detail:

Let’s start with the largest position first, the now so famous Alibaba stake. From a technical perspective, Softbank doesn’t own the listed shares but this: