Short cuts: KAS Bank, April SA, Draegerwwerke GS

KAS Bank

When I invested into KAS Bank, the Dutch, the main motivation was the cheap valuation and the stable core business (custody). One add-on was that they wanted to extend their retail business together with dwp bank from Germany.

For some reason, dwp decided not to go ahead with this cooperation and cancelled it in June 2014. Kas Bank will be compensated for this according to the press release:

As a compensation for the loss of the anticipated annual saving that KAS BANK would have realised from 2016 onwards, dwp bank will pay KAS BANK a lump sum at the end of June which, after deducting the costs in 2014, amounts to approximately € 20 million. KAS BANK will use this one-off compensation to invest in further improving its efficiency and its services to institutional investors. dwp bank will focus its future investments on improving the quality and standards of its operations and IT.

20 mn compensation for a 160 mn Market company is a lot, but it seems that this contract would have been quite good for KAS Bank going forward. Maybe it was so good that dwp bank only recognized it after signing ? I don’t know. In any case, I think the “Value case” for KAS Bank is still intact. Book value should still be achievable, which would mean the stock has still 50% upside let, despite the quite satisfactory performance of +58% (incl. dividends) since I bought the stock 2 years ago.

April SA

A few weeks ago, I finally sold the rest of my April SA position. I never really explained this in more detail. When I first looked at April SA, I didn’t buy it because the stock was not cheap enough (part 1, part 2, follow up, follow up).

I only established a position when the stock got hammered during the EUR crisis, as they were then trading in single digit P/E territory and implcitly I asumed at least constant earnings going forward. Fast forward 2 years. EPS developed negatively, both in 2012 and 2013:

| EPS | |

|---|---|

| 31.12.2010 | 1,96 |

| 30.12.2011 | 1,37 |

| 31.12.2012 | 1,32 |

| 31.12.2013 | 1,26 |

Nevertheless, the new-found enthusiasm for European and especially French stocks led to a significant multiple expansion from around 8xP/E to ~ 14xP/E in June. Although I still think that April is not a bad company, I had to admit that the ~63% return I made on the stock was much more luck than anything else as I don’t think that multiple expansion like this (even considering shrinking EPS) could be forecasted. Additionally, I found much more interesting alternatives in the insurance sector (Admiral, NN Group), so I decided to sell although the two years holding period were shorter than I would normally target.

Draegerwerke GS

A few days ago, Draeger revised their guidance for 2014 significantly downwards. The stock got hammered significantly, the Genußscheine lost some value as well but less than the shares.

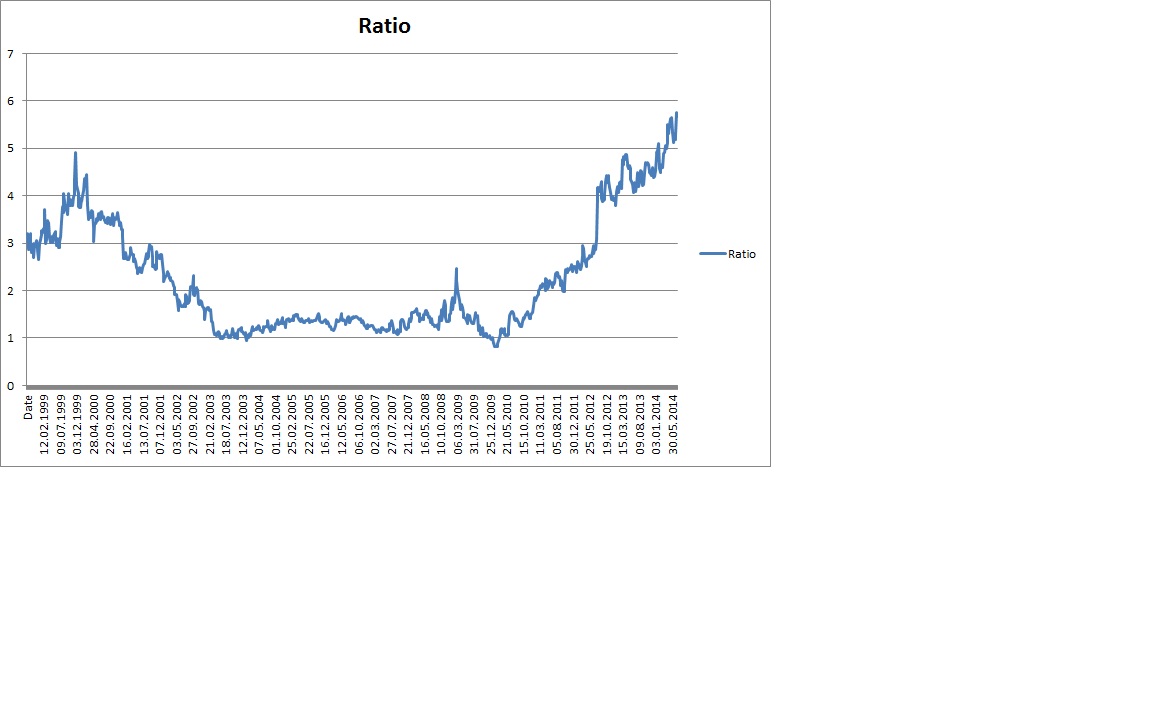

For me, Draeger was always a relative bet, assuming that the intrinsic value of the Genußscheine (10 times the Vorzuege) would at sometime close. I never believed that Draeger itself was a “great” company. Looking at the developement of the ratio (price Genußschein / Price Vorzuege) we can clearly see that currently we are in a territory which we haven’t seen for the last 15 years:

At almost 6 times the Pref shares, the relative risk/return ratio is not as good as it was before. With almost 7%, the Draeger Genußschein is still with a margin my largest position. In order to reflect the somehow lower relative potential of this position, I will cut the position to a 5% stake going forward.